On This Page

Purchase of New Site

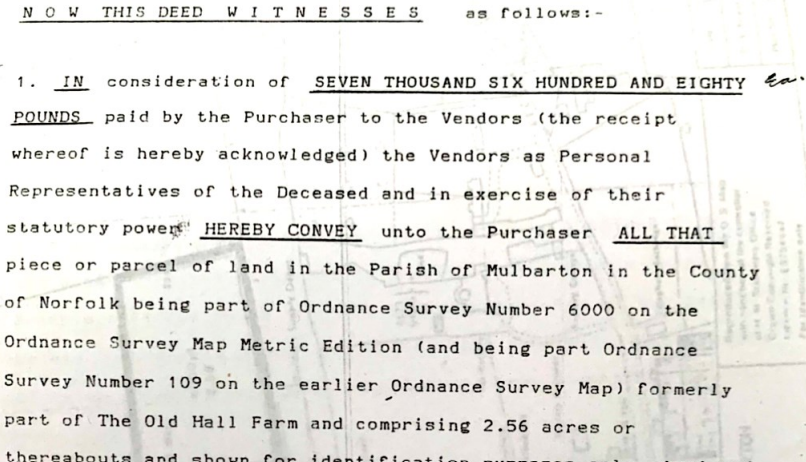

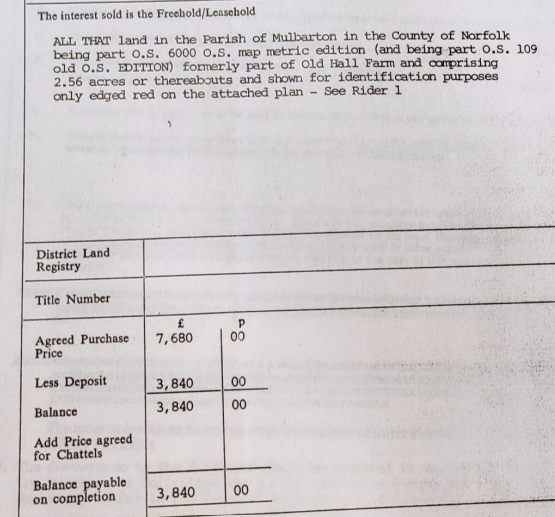

In December 1985, Mulbarton Parish Council purchased the 2.56-acre site on which the present village hall was later built. The contract of sale and conveyance name the Parish Council as purchaser and legal title holder.

At the time of this purchase, the Village Hall charity was still operating from the Old School site, and the process of planning a replacement hall was ongoing.

Funding the New Hall

In 1983, residents were asked to vote in a parish referendum on whether to significantly increase the parish precept to fund a new village hall.

The proposal was to increase the precept from approximately 2p per household per day to around 5p per household per day — an increase of around 250%.

Approximately a quarter of residents participated in the vote, with over 97% voting in favour. This provided a substantial and ongoing funding stream, raised specifically for the purpose of delivering a new village hall for the parish. These funds were then used by the Parish Council in the years that followed, including to purchase the 1985 site.

When construction was complete, the Charity had been so successful at self-funding the £350,000 build, there was £30,000 of precept-generated income left over. The Parish Council re-directed this to other projects.

Early Planning and Governance Discussions

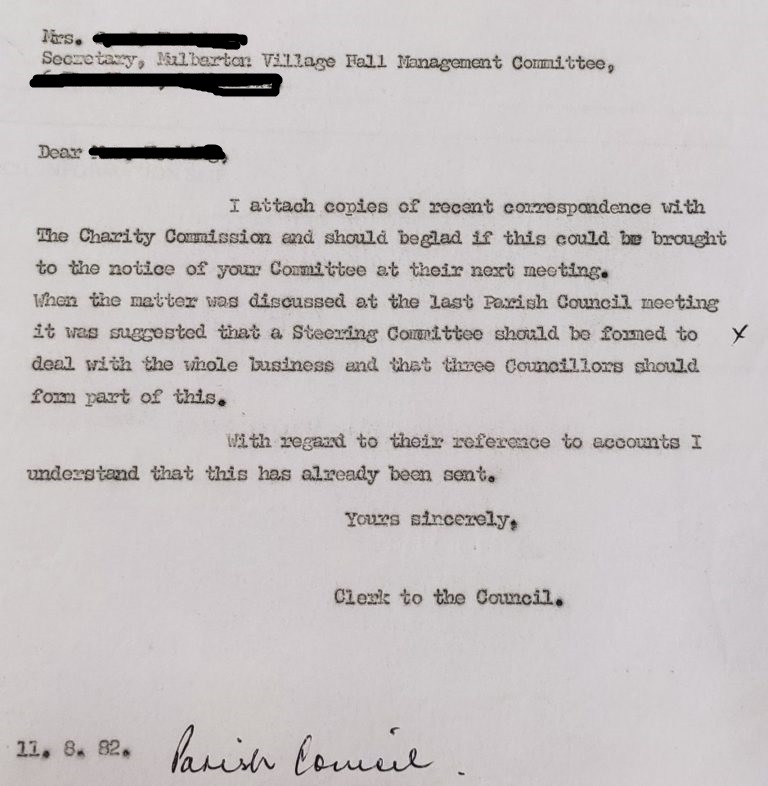

By 1982, discussions were already underway about the future of the existing hall and the possibility of building a new facility.

In correspondence from that year, the parish clerk provided the Village Hall management committee with copies of communication with the Charity Commission and noted that a steering committee was to be formed, including parish councillors.

Steering group records from 1986 show that key questions about governance and ownership were being actively considered during the planning phase.

Minutes from February 1986 record:

“The proposed new centre must have charitable status, and the Charity Commissioners to be contacted about the sale of the existing Village Hall.”

A memorandum from the same period raises the need for clarity about roles and ownership:

“It is most important to be clear on the relative status of the Village Hall and the Parish Council… one must be clear that the titular owners of the Community Centre would be the Trustees of the Village Hall.”

Another memorandum warns the Parish Council of potential legal difficulty, regarding the plan to invest the proceeds of sale from the existing charity property:

Skip to PDF content“…you may be relying on a sum of money to which you have no legal right.”

These records show that charitable status, ownership, and the relationship between the Parish Council and the Village Hall charity were recognised as important issues before the new hall was built.

Funding Structure and VAT

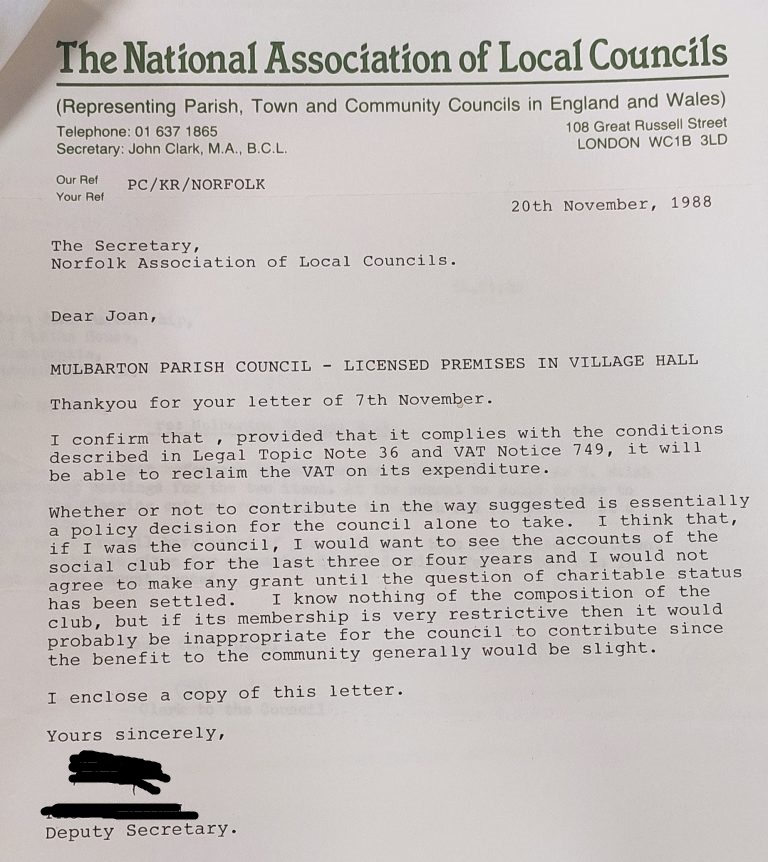

Correspondence from 1980 onwards shows that Parish Council funding and VAT recovery were part of the developing approach to village hall provision.

Letters from 1980 record that:

- the Village Hall would receive financial support from the parish precept; and

- VAT-bearing expenditure could be routed through the Parish Council’s accounts so that VAT could be reclaimed.

A later advisory letter confirms that, provided the relevant conditions were met, the Parish Council would be able to reclaim VAT on expenditure connected with the project.

To recover VAT, the conditions mentioned in the correspondence stipulate that the Parish Council had to receive “nothing in return”, in exercise of their power from s.133 of the Local Government Act 1972, to give financial assistance to a Village Hall Charity. This is because VAT is a tax on value added, so is only recoverable if no value is added.

These arrangements formed part of the financial structure supporting the development of the new village hall, which relied on the new property being held in trust, in the same way as the Old School site, and the Parish Council receiving no interest in the property – “nothing in return”. Altogether, almost £12,000 VAT was recovered from the construction costs of the Village Hall in 1989.

The Position in 1985

The 1985 conveyance documents show the Parish Council acquiring legal title to the new site.

At the same time:

- residents had approved, through referendum, the raising of funds specifically for a new village hall;

- the existing Village Hall charity continued to operate;

- planning for a replacement hall was underway; and

- contemporaneous records show that charitable status and governance arrangements were being actively considered.

The 1985 documents therefore form part of a wider sequence of events, rather than a complete statement of how the new site was to be held or managed.

In Short

The Parish Council purchased the current village hall site in 1985 and holds legal title to that land.

The purchase followed a parish-wide referendum in 1983, in which residents overwhelmingly supported raising funds through the precept to provide a new village hall.

Records from the period show that charitable status, governance, and the relationship between the Parish Council and the Village Hall charity were under active consideration as the project developed.

Subsequent documents (covered in later pages) address how the transition from the Old School hall to the present site was carried out.

Leave a Reply